24 April 2025

Global markets are currently experiencing more volatility, largely due to geopolitical developments and US trade (tariff) policy. It's natural to feel concerned about how your super is performing. But it’s important to remember that market ups and downs are a normal part of investing.

While market volatility may be more noticeable in the short term, for most members, super is a long-term investment. AustralianSuper has a team of investment specialists who are experienced in actively managing member money through different market conditions and events.

AustralianSuper has substantial liquidity and reserves to fund payments to members and to invest in opportunities as they arise.

Frequently asked questions

-

Why has my balance dropped?

Global markets are experiencing more volatility, largely due to geopolitical developments. This is mostly centred in the US where the new Trump administration has begun implementing trade policies. We understand it can be unsettling to see your balance fall. Market ups and downs are a normal part of investing and volatility is more noticeable in the short term. That’s why it’s important to look beyond the short term. Even members in or approaching retirement can still be invested for another 20 or more years.

-

What is AustralianSuper doing to manage this?

As a long-term investor, we review and adjust the portfolio in response to the changing economic and market outlook and actively seek opportunities to deliver value for members.

Our investment teams are monitoring ongoing developments of trade policies and assessing the potential impacts on asset markets and how to best position the portfolio to deliver long-term performance.

-

Should I make changes to how my superannuation is invested?

It’s important to remember that your super is a long-term investment, even for most people in retirement. While changes in your balance can be worrying, market fluctuations are normal (as we can see from the impact of market cycles on asset classes) and that’s why keeping a long-term focus is important.

If you make decisions based on short-term considerations, you could end up worse off in the long run. This includes activities like switching investment options which can have a significant impact on how much super you’ll have when you retire.

When it comes to investing through super, you have choices, our risk profiler may help you to work out the type of investor you are, so you can be better guided when making investment decisions.

-

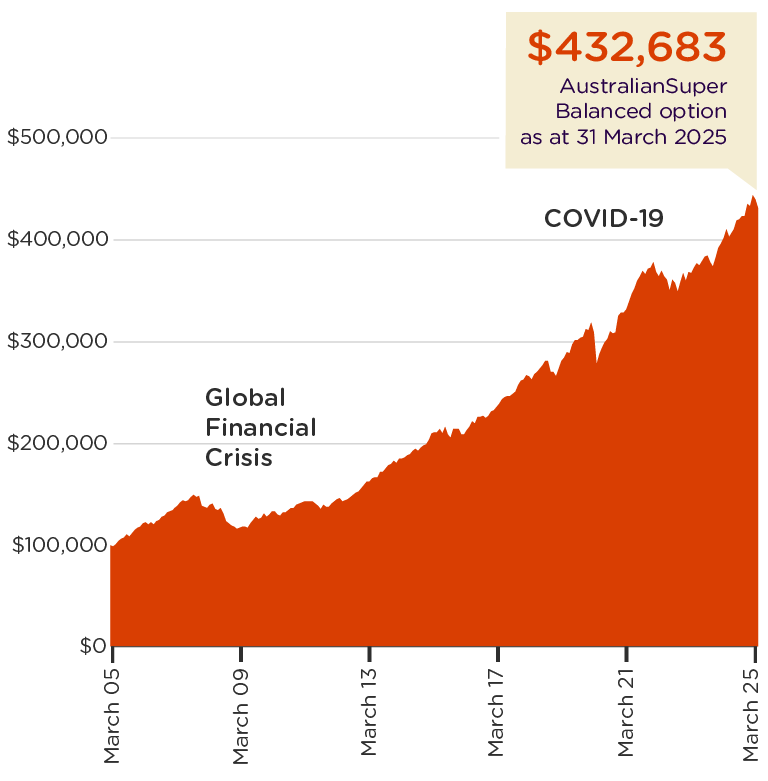

How has the Balanced option (Super) performed over the long term?

This chart shows the growth of $100,000 invested in the Balanced option over 20 years to 31 March 2025. Over this time, without any additional contributions, $100,000 has grown to $432,683 – despite market ups and downs.

Growth of $100,000 invested in Balanced option (Super) from 31 March 2005 to 31 March 2025

AustralianSuper investment returns are based on crediting rates, which are returns less investment fees and costs, transaction costs, the percentage-based administration fee deducted from returns from 1 April 2020 to 2 September 2022 and taxes. Returns don’t include all administration, insurance and other fees and costs that are deducted from account balances. Returns from equivalent investment options of the ARF and STA super funds are used for periods before 1 July 2006. Investment returns aren’t guaranteed. Past performance isn’t a reliable indicator of future returns.

-

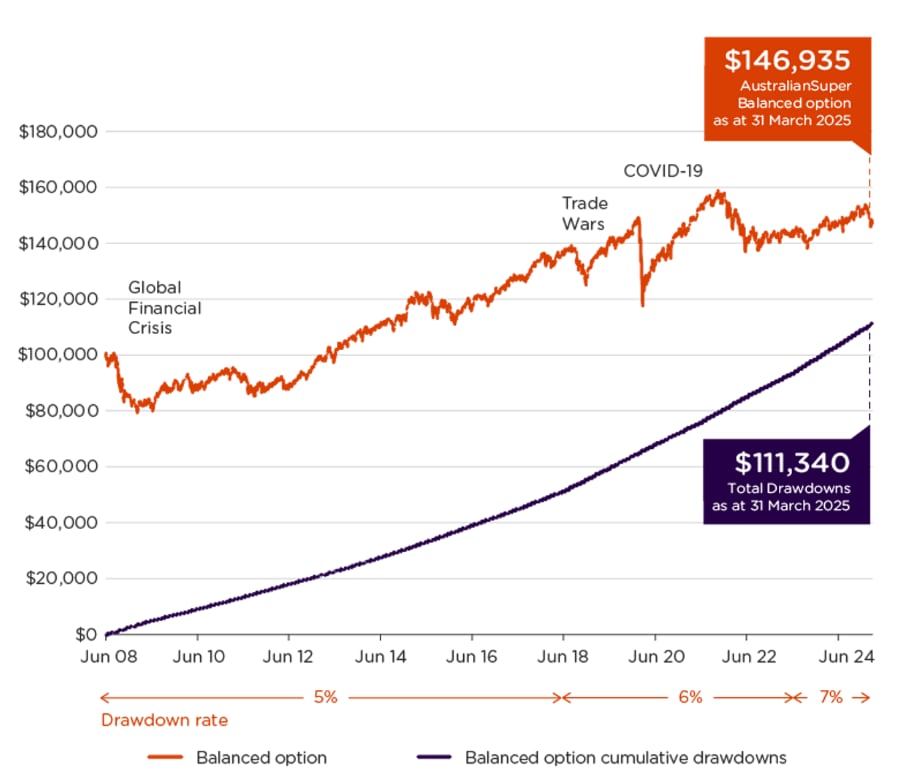

How has the Balanced option (Choice Income) performed over the long term?

This chart shows the growth of $100,000 invested in the Balanced option for Choice Income, from 30 June 2008 to 31 March 2025. Over this time, without any additional contributions, $100,000 has grown to $146,935 – despite market ups and downs and $111,340 in total drawdowns.

Growth of $100,000 invested in Balanced option (Choice Income) from 30 June 2008 to 31 March 2025

Assumptions: Starting age: 65; Drawdowns: Starts at 5% of the year-end balance and increases with age, based on current minimum rates. AustralianSuper investment returns are based on crediting rates, which are returns less investment fees and costs, transaction costs and taxes. Doesn’t include all administration and other fees and costs that are deducted from account balances. Investment returns aren’t guaranteed. Past performance isn’t a reliable indicator of future returns. Source: AustralianSuper Minimum rates available from the ATO: ato.gov.au/tax-rates-and-codes/key-superannuation-rates-and-thresholds/payments-from-super

-

What is a bear market?

When share market values are falling over a prolonged period of time, it’s known as a bear market. They are often associated with major economic downturns, like the Great Depression in the 1930s and the Global Financial Crisis in 2008/09. The technical definition of a bear market is when asset prices have fallen by more than 20% from their recent highs.

-

What may happen to your super in a bear market?

If share prices are falling, your super may experience a fall in value too. In that scenario, some members might think that moving from a diversified investment option such as AustralianSuper’s Balanced option to a cash option would avoid further falls. If you’re thinking of switching, it's important to understand the risks and check before you switch, and also to consider your financial advice options1.

1 Personal financial product advice is provided under the Australian Financial Services Licence held by a third party and not by AustralianSuper Pty Ltd. Fees may apply.

-

What is a bull market?

A bull market is when investor confidence is strong, and prices are rising faster than average over a consistent period. Bull Markets typically (although don’t always) coincide with periods of strong economic growth, and investors are attracted to the potential of higher returns.

-

What may happen to your super in a bull market?

During a bull market, the share market value is rising, and your super may grow too. During a rising share market, you may be considering if what you’re invested in is right for you. To find out more about the right investment option for your specific needs, visit Choosing the right super option. With changing conditions, it’s worth understanding the risks of switching over the short term. It’s good to understand that super is a long-term investment to help you reach your best retirement outcome.

Our Balanced investment option is designed to have medium to long-term growth with possible short-term fluctuations. It is recommended that this option has a minimum investment timeframe of at least 10 years.